- Despite the market ructions witnessed in February, nothing seems to deter investors for long. A strong cyclical backdrop and robust earnings growth seem to forever ratify the prevailing ‘Buy the Dip’ mentality.

- Yet, take a step back and you can see momentous transformations taking place. Markets have digested their initial shocks well, but these may simply represent the vanguard of a much broader shift in the prevailing investment paradigm.

- These tectonic shifts may not immediately affect asset prices, but they will eventually reach a point at which they could fundamentally alter the way investors view, and value, risk assets.

- As a result, it is time to scale back risk, in particular in US equities and long term rates.

Definition: A fundamental change in approach or underlying assumptions

Despite a sharp correction in the US stock market in February, nothing seems to deter investors for long. The S&P 500 is now up for the year and other than a rise by less than 50bps in government bond yields and slightly more realistic volatility readings, not much else seems to have changed.

Yet, like with background radiation, all is not what it seems. To be sure, the cyclical backdrop remains robust. Growth may be moderating somewhat and fall short of rising expectations, but it remains firmly above trend. Similarly, inflation readings are moving higher, but still fall short of central bank targets. The Fed appears to turn more hawkish, but monetary policy will remain accommodative for some time, with the Federal Funds rate remaining below the neutral 3% level even if the Fed delivers four rate hikes in 2018. Despite some adjustments to the cyclical outlook, the backdrop thus remains benign and corporate earnings expectations strong.

However, investors have also encountered a series of shocks recently, which may represent the birth pangs of a broader change in the prevailing paradigm (a concept similar, but slightly different to Robert Shiller’s recent work on “Narratives“). This has been an iterative process and markets have weathered the shocks well so far. But eventually the cumulative effect of these shocks will reach a critical point, at which they could affect investment strategies more permanently. Several key assumptions that have underpinned the world economic and political order for about a generation have begun to unravel as of late, most importantly the notion of a continuous drive toward a free-market, liberal order of the world. Specifically, this comprises the following ‘mega-trends’:

- The Death of (Right-Wing) Populism: The election of Donald Trump, the strong electoral showing of the AfD in Germany, the increasingly authoritarian leadership in Poland and Hungary, the Far Right’s participation in the government of Austria and the victory of M5S in the Italian election amongst others suggest that populism is alive and well and that protest votes can easily turn into support for illiberal or more nefarious ideologies. At the same time, the emergence of the radical left (Jeremy Corbyn in the UK, Bernie Sanders in the US) suggests that populism is not necessarily confined to the right-wing side of the political spectrum.

- An Ever-Closer European Union: The failure by member states to adhere to fiscal rules, the rejection of agreed common immigration rules, the emergence of a less cooperative “Visegrad” bloc, and last-but-not-least the Brexit vote have made it clear that ever-closer union is far from a foregone conclusion.

- The US, Champion of Free Trade and International Cooperation: The pull-out from the TPP agreement and of the Paris Climate Accord, criticism of NATO and the UN, and the recent imposition of trade measures point to a retrenchment of the US from the post-war global order and its cooperative structures it was instrumental in building.

- China on the Path Towards Democracy: China’s ambitions to remodel its economy have long been assumed to be the precursor to a move towards a more liberal and democratic political system. The recent removal of term limits for the president suggests that the direction of travel is instead towards strengthened authoritarianism and state control of the economy.

- Interest rates in Long Term Decline: Interest rates have been in decline for over 30 years as the Fed beat back inflation and then turbo-charged the process with its unconventional policy measures following the 2008 financial crisis. This development has begun to reverse with five rate hikes in this cycle and the upward pressure on long term rates exercised by the Fed’s balance sheet reduction as well as the administration’s extraordinary fiscal expansion. In addition, new Fed Chair Powell has poured cold water on the markets’ assumption of an implicit ‘Fed Put’.

These gradual tectonic shifts in the market backdrop may not immediately affect asset prices, but they may coalesce over time into a less benign environment that fundamentally alters the way investors view, and value, risk assets. More specifically, the waning ‘Fed Put’ could lead to higher short term rates and curve flattening in the near term. On the other hand, the Trump administration’s unprecedented fiscal expansion (outside times of war or recession) and the Fed’s balance sheet reduction could steepen the curve again, resulting in an altogether shift higher of the entire yield curve. If the trade sanctions imposed by the US (thus far insignificant from a macroeconomic perspective) invite retaliation and escalate into a full-blown ‘trade war’, it could weaken the dollar and lower earnings, weighing on the stock market. Finally, China’s drift towards greater authoritarianism raises the risk of policy mistakes and a more confrontational stance with the West.

The Inflation Bogey

There are certainly many other, ‘volatility enhancing’ developments which could affect investor sentiment or the broader market landscape not discussed previously. They include the threat of long-term military conflict in the Middle East (Syria, Saudi-Iranian proxy wars, pre-emptive strikes by or on Israel) or Asia (North Korean attacks on the South or Japan, pre-emptive US strikes), the sharp rise of global debt in the wake of the Global Financial Crisis, the rising issuance of IPOs with no voting rights, the rollercoaster ride of cryptocurrencies, ICOs etc.

But one of the most enduring fears is that of a rise in inflation. Yet, inflation has been and remains a chimera. Long alarmed by the putative hyper-inflationary implications of central bank balance sheet expansions, market participants have only just stopped worrying about the threat of deflation. Meanwhile, US Core PCE remains at a well-behaved 1.5% yoy (February) and hasn’t touched the targeted 2% level since 2012. The blip in in US wage growth (average hourly earnings) to 2.9% yoy in January was a weather-related fluke that reverted to 2.6% yoy a month later.

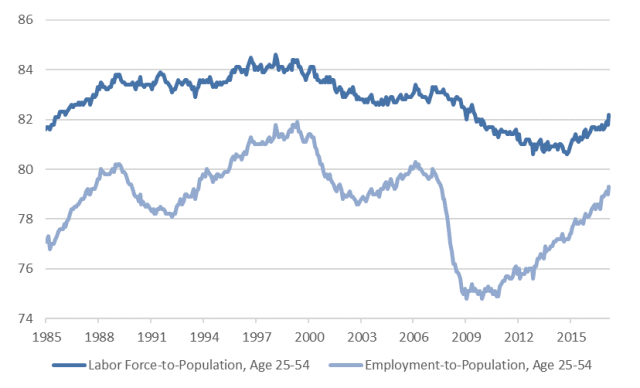

Indeed, while the US economic expansion is now long in the tooth, it remains some distance from facing any internally generated inflation pressure. The ongoing recovery continues to suck people of working age who were previously thought structurally unemployed back into the labor force, keeping a lid on general wage demands. But while the labor force (the number of employed and unemployed persons) expands, its size remains significantly smaller than during previous decades (see chart). Similarly, the number of employed persons has increased rapidly, but remains below the levels recorded prior to the technology bust. The unemployment rate has decreased rapidly (shown as the difference between the two series in the graph below), but this presents a misleading picture. In fact, the economy remains farther from full employment than the decline in the unemployment rate suggests. And with more slack in the economy, inflation pressures are kept in check. While it is true that a return of meaningful inflation pressures could alter the investment landscape radically, such a threat remains absent for now.

The Bottom Line: Scale Back Risk

The paradigm change is underway, yet markets continue to trade as they have in the past few years (‘buy the dip’). The realization that a new environment is upon us may not take hold in the near term as cyclical factors remain strong and corporate earnings growth robust. But the adjustment is unlikely to take place in a linear fashion. Once it does take place, it will likely create a sharp discontinuity in asset prices.

How to position for this? For now, the latest developments speak more to fixed income- than to equity markets. What is more, the short end of the market has already moved a good deal and is unlikely to move that much further given 1) the gradual approach of the Fed to rate hikes, 2) the lower level of the terminal rate and 3) the residual uncertainty with respect to the cycle. On the other hand, the long end is subject to a multitude of negative factors and thus less attractive than the short end.

For equity markets, it would take much higher inflation and interest rates than currently to dent the earnings outlook. But US stocks also suffer from an exceptionally long rally, a boom in tech stocks and elevated valuations. It is worth paring back risk exposure in US equities and credit now in order to avoid the possibly destructive effects of a non-linear adjustment in market perceptions.

{kind=link}