- As ECB policy rates skirt the zero bound, expectations for the use of alternative tools, such as negative deposit rates are again on the rise. However, this is an ineffective and potentially harmful policy option.

- Several problems may arise: transmission across other rates in the financial system is not guaranteed, bank profitability would almost certainly suffer, logistical problems could arise from a massive shift into physical cash and , most importantly, the ECB’s balance sheet would contract, just when the opposite is required.

- More useful would be measures aimed at the de-fragmentation of EZ financial markets, such as a selective asset purchases or lending against a differentiated set of collateral rules.

- Yet, it is questionable whether policies targeted at reigniting lending are sensible at all when the private sector is in a de-leveraging phase and impediments to growth are primarily structural.

With its latest 25bps cut, which took the benchmark two-week refi rate to 0.25%, the ECB has almost completely exhausted its conventional policy tool kit. As a result, the need to resort to more “unconventional” policy measures has become increasingly pressing. The ECB is certainly no stranger to such an approach: while it has been loath to adopt a policy of quantitative easing (QE) like some of its peers, it has changed its modus operandi in several respects throughout the crisis – between May 2010 and February 2012 it purchased Eur200 bn worth of peripheral sovereign debt under the Securities Markets Program (SMP), in December 2011 it introduced Long Term Refinancing Operations (LTROs) with a term of up to 36 months, it changed its liquidity provision to a “full allotment” procedure (providing all the liquidity demanded), eased its collateral requirements and eventually announced a new – but yet untested – program of Outright Monetary Transactions (OMT) in September 2012.

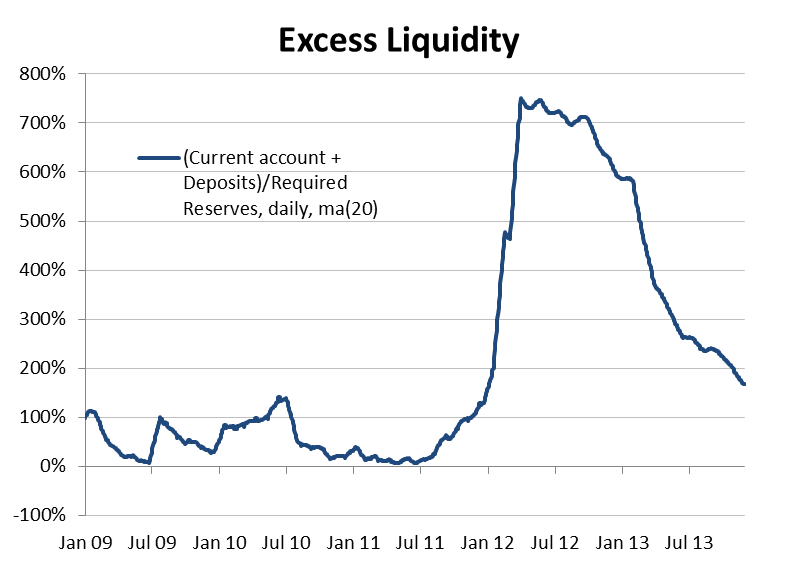

Yet, while these and the many other measures adopted may have helped forestall an even worse outcome, they failed to unclog the financial system and reignite bank lending (let alone wider activity). This is clearly evident from the lack of growth of private lending data as well as the sharp and ongoing decline in the money multiplier (see chart).  A common explanation is that this was due to risk averse banks hoarding cash on the central bank’s balance sheet, Indeed, a “fear gauge” that measures bank holdings as a proportion of liquidity provided shows a sharp increase from the 50-60% observed until mid-2011 (similar to their US counterparts) to close to 100% by year-end 2011. The ECB’s attempt to “push” deposits off its balance sheet by reducing the deposit rate to 0% in July 2012, simply led to an immediate and commensurate increase in bank current accounts (which we described here). For this reason, “bank holdings” as defined in Chart 2 represent the sum of bank deposits and current accounts at the ECB. With the rate on current accounts at 0.5%, banks can happily park their cash there and it is thus no surprise that excess reserves (those held beyond required reserves and so-called autonomous factors) still stand at over 160% of required reserves (see Chart)

A common explanation is that this was due to risk averse banks hoarding cash on the central bank’s balance sheet, Indeed, a “fear gauge” that measures bank holdings as a proportion of liquidity provided shows a sharp increase from the 50-60% observed until mid-2011 (similar to their US counterparts) to close to 100% by year-end 2011. The ECB’s attempt to “push” deposits off its balance sheet by reducing the deposit rate to 0% in July 2012, simply led to an immediate and commensurate increase in bank current accounts (which we described here). For this reason, “bank holdings” as defined in Chart 2 represent the sum of bank deposits and current accounts at the ECB. With the rate on current accounts at 0.5%, banks can happily park their cash there and it is thus no surprise that excess reserves (those held beyond required reserves and so-called autonomous factors) still stand at over 160% of required reserves (see Chart)

A brief list of arguments

This represents a first – albeit admittedly limited – argument against a further cut in the deposit rate (into negative territory): funds would simply shift to current accounts. A move to negative rates could only be meaningful only if holdings on current accounts were simultaneously penalized (be it through quantitative restrictions or an equivalent rate).

More importantly, in an article in mid-2013, Gavyn Davies presented a series of practical problems with negative deposit rates that are worth recalling:

- The idea of introducing negative interest rates in general is the same as that of reducing interest rates – to shift future private consumption into the present. For this to occur it is necessary that the lowering of the policy rate permeate the entire financial system. This is where potential problems could arise: at – or below – the zero bound things start to behave differently. The argument has been made that a move into negative territory could drain liquidity in the market and that money market rates might not follow policy rates down. However, the Danish experience has shown that money market rates can indeed go negative, although they also became more volatile (the Danish central bank lowered its deposit rate to -0.20% in July 2012, then raised it to -0.10%).

- Similarly, if banks do not pass on negative rates to customer deposits, this could lead to an unwelcome compression of profit margins. And if alternatively they were to raise their lending rates to restore profitability, it would represent a perverse effect of monetary easing.

- Another concern is that a cut to -0.25% would probably be the last one as any further move would simply induce banks to hold physical cash. This in turn could lead to logistical problems. There might also be technical problems in the repo market for government bonds due to a lack of liquidity.

However, there are also broader policy issues that make negative interest rates an inadequate policy instrument:

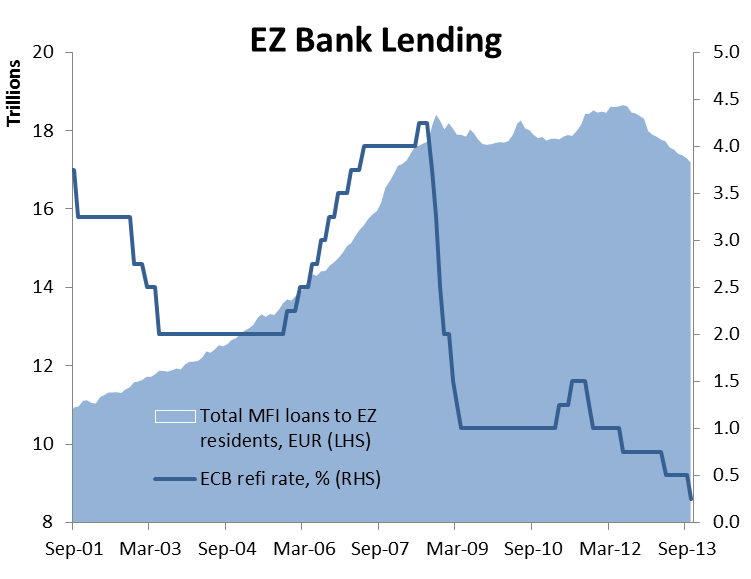

- Most important is the fact that the clogged credit channel in the EZ owes not to an insufficiently low level of interest rates but to 1) regulatory changes and increased risk aversion on the lenders’ side which constrain the supply of funds and on the other hand, 2) a lack of demand for funds from de-leveraging corporate and household sectors. It is unlikely that a 25bps reduction in the bank deposit rate will induce a transformative behavioral change in the economy, when a decline in the deposit rate from 3.25% in 2008 to 0.0% in mid-2012 has not (see chart).

- Negative rates are contractionary in nature. Thanks to sizable LTRO repayments, the ECB balance has already contracted 26% since it reached a peak of Eur3.1 trn in June 2012. This is a development that goes in the wrong direction. Granted, aggregate balance sheet expansion is a blunt instrument, but it still benefited the financial system in the peripheral economies while banks in the core economies broadly opted out of assistance. Indeed, German banks have already repaid 100% of their LTRO loans, while Spanish and Italian banks have only done so to the tune of 45% and 13% respectively. All else being equal, negative interest rates on deposits would lead to a further decline of the ECB’s balance sheet and thus a shrinking in broad money, unless they spark a radical behavioral change.

What are the alternatives?

Any central bank has a variety of policy options, even at the zero bound. Instead of acting directly on the price of money, it can act on the quantity of money. Asset purchases are the most direct way of doing so and the central bank can become more aggressive in easing, the further it goes out the risk spectrum (eg purchasing private loans or equities). The ECB could choose to go down this route and become more selective, without being accused of bankrolling governments.

Along similar lines, the ECB could lend to lend to member states selectively, by launching a new set of LTROs and configuring collateral requirements such that they primarily incentivise banks in peripheral economies to participate. Ultimately, the ECB could also engage in a generalized quantitative easing program similar to other central banks. But given the heterogeneity of the currency area over which it presides, this represents a particularly crude tool.

Finally, one has to ask how much power the central bank has in the face of such a systemic and structural crisis altogether and whether policy action is fundamentally called for. Now that the EZ has escaped the most virulent stage of the crisis, the task has shifted from avoiding the break-up of the currency union and managing default/restructurings to reigniting growth. Given that the impediments to growth in the Eurozone are primarily structural (eg labor markets, productivity, tax systems), the ECB’s powers are quite limited. What is more, to the extent that excessive credit taking represented a key sources of the crisis, stimulating borrowing seems ill-advised in a period of private sector de-leveraging.