- Bill Gross argues that credit is losing its power and suffers from entropy, destined to a fatal supernova end. But pay heed to the power of compound interest and the fact that correlation does not establish causation and it is clear that PIMCO’s analysis is nothing but a fallacy of galactic dimensions.

PIMCO has an investment (and AUM) record that is the envy of many market participants. So it is with some justifications that they occasionally pontificate aloud and introduce grand notions like ‘secular trend’ and the ‘new normal’ into the mainstream financial jargon. But this time Bill Gross, Co-CEO of Pimco, has outdone himself: not content with history a few hundred years long, he takes the long view. The really long view. A few trillion years to be exact. And he likens the development of the world’s financial system to the implosion of a supernova.

Now, there is a lot to be said for Hyman Minsky’s theory of credit cycles which Bill Gross freely invokes in his article. In fact, it fairly accurately describes what happened over the past decade plus. What is more, Minsky had the insight to come up with all this some 30 years before time. But Gross takes his theory to the extreme, arguing that the there is an underlying secular trend (sic!) in credit cycles so that even when they unwind (deleveraging), they never do so completely and there is in fact a drawn out ‘ratcheting effect’ (a mundane analogy by yours truly). He claims that just like in the universe, credit markets are characterised by a rising degree of entropy (heat dissipation or loss of energy) and are therefore destined for an irrevocable demise (he is a bit fuzzy on the timing on that one).

What this all boils down to is the following:

“Each additional dollar of credit seems to create less and less heat. In the 1980s, it took four dollars of new credit to generate $1 of real GDP. Over the last decade, it has taken $10, and since 2006, $20 to produce the same result. […]This “Credit New Normal” is entropic much like the physical universe and the “heat” or real growth that new credit now generates becomes less and less each year: 2% real growth now instead of an historical 3.5% over the past 50 years; likely even less as the future unfolds.“ (original emphasis)

Now there is a fallacy – compounded by erroneous thinking – if you ever saw one!

Let’s start with the easy part: it’s inflation, Bill! At 2.5% inflation per year, the force of compound interest means that prices will have risen by nearly 110% over 30 years (the actual average CPI since 1980 in the US is 2.4%). In other words, what cost $4 in 1980, requires $8.3 today. So we are comparing a nominal variable – credit – with a real (ie inflation-adjusted) one, real GDP growth.

Secondly, correlation does not imply causation. You would hope that the Masters of the Universe who manage our hard-earned money know that. Growth slowed and credit expanded – does that mean that growth cannot accelerate without a further pick up in credit growth? Does it mean that growth is caused by credit? Or could growth be driven by other factors (economists like to point to labor input, capital accumulation, technological change and consequent productivity gains)? To wit, could it even be that the reverse is the case, ie that rapid economic expansion coupled with legislative and institutional changes allowed credit to surge?

It is clear that there are many candidate explanations for both the acceleration and the deceleration of economic growth. Anyone familiar with monetarist theory would not count the creation of money, aka ‘veil’, amongst them (a Nobel Prize has been awarded to one Milton Friedman after all). The coincidence of credit growth with economic growth simply does not establish anything. One might as well relate the rise in the earth’s temperature or the increase in the world’s population over the same period to the growth of credit. For the galactic argument’s sake: even Halley ’s Comet appeared twice in the 20th century (1910 and 1986) after showing up only once in both the 19th and the 18th century (1835 and 1759). Is that due to the rapid expansion of credit?

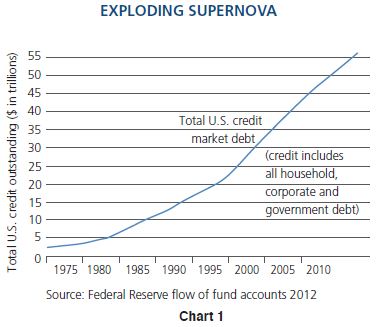

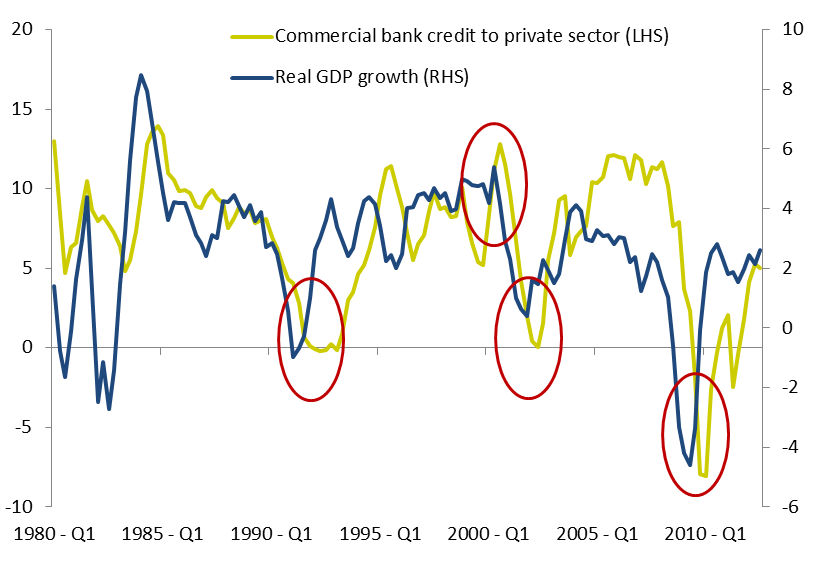

You can probably see where this is going. But stay with it. Gross tries to impress his point upon us with Chart 1.  But I would suggest that Chart 2, which we have produced, is the more pertinent one. It shows the growth of real GDP and private credit in the US since 1980. At first glance it suggests a broad correlation over the period. Yet, the correlation coefficient of the two series is a mere 32%. The reason for this is readily apparent: look closer and you’ll see that year-on-year credit growth clearly lags GDP growth (check the peaks and

But I would suggest that Chart 2, which we have produced, is the more pertinent one. It shows the growth of real GDP and private credit in the US since 1980. At first glance it suggests a broad correlation over the period. Yet, the correlation coefficient of the two series is a mere 32%. The reason for this is readily apparent: look closer and you’ll see that year-on-year credit growth clearly lags GDP growth (check the peaks and  troughs). This implies a rather different causation: that it is a downswing in activity that impairs the demand for credit and thereby slows it space of expansion. Of course, this is just a hypothesis and the correlation doesn’t establish it, as we have argued. But it is just as plausible as the one our trusted Pimco advsiors suggest. Minsky’s theory has a lot of merit, but hold off on supernova trades for now.

troughs). This implies a rather different causation: that it is a downswing in activity that impairs the demand for credit and thereby slows it space of expansion. Of course, this is just a hypothesis and the correlation doesn’t establish it, as we have argued. But it is just as plausible as the one our trusted Pimco advsiors suggest. Minsky’s theory has a lot of merit, but hold off on supernova trades for now.