- The numbers involved are small. Yet, the Troika/Cyprus move to renege on deposit insurance and appropriate private funds is set to reverberate beyond the tiny island.

- The decision bodes ill for future rescue efforts: 1) it derails popular support for any adjustment plan, 2) it reveals the ECB’s promise to do “whatever it takes “ and engage in unlimited OMTs as an empty bluff, 3) it puts the nail in the coffin of the putative European banking union and 4) it turns the plan to create a well-understood resolution regime and creditor hierarchy on its head.

- All these serve to undermine the credibility and hence the efficacy of any future rescue attempt in the Eurozone.

Call it sequestration, expropriation, default or a bank levy. All of these ring true in economic terms but legally speaking, the latest move by the troika and Cyprus designed to top up a Eur10 bn bail-out package for its banks is merely a tax. And not a particularly onerous one at that: 6.75% (or less) on deposits of less than Eur100 000 and 9.9% (or more) on deposits of more Eur100 000. What is more, all this takes place in a tiny economy of a divided island that constitutes a mere 0.2% of Eurozone GDP. So why all the fuss?

The EU is right in arguing that in some ways the Cyprus case is special and hence the hit to (retail) depositors need not be a feature of future financing deals elsewhere:

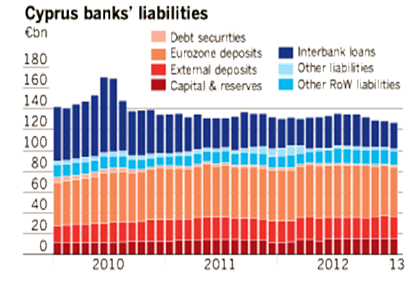

- Uniquely in the Eurozone, Cyprus’ banking sector is huge at eight times GDP;

- The majority of the local banking sector’s liabilities consists of deposits, not bonds;

- An unusually large share (45%) of these deposits is owned by foreigners.

But the move is nevertheless troublesome in several significant ways and underscores the paucity of policymaking in the Eurozone, in particular when market pressure appears to be off, letting politicians hang back and take a gamble.

First, the decision is politically disastrous in that it 1) breaks with existing insurance guarantees for depositors, setting a negative precedent and 2) is a highly regressive move that hits small savers the most. This in turn undermines any political support the government might have had, amidst an environment in which voters everywhere drift to extremist and fringe parties.

Equally importantly, it flies in the face of the two pillars of EZ policy that have underpinned the stabilization of market sentiment over the past nine months: the ECB’s promise of OMTs and the progress made – however tentative – towards a banking union.

One of the key features of the EZ crisis so far has been the nefarious nexus between the sovereign and the banking system. The initial transmission channel ran from the sovereign to the banks as the latter were the key holders of government securities and their stock had risen to unsustainable levels (indeed, it was the Greek debt restructuring that got Cypriot banks into trouble). The ECB managed to sever this link through the provision of unlimited liquidity to (solvent) private banks via its 3yr and other LTROs in 2011/12.

But it cannot sever the transmission channel from banks back to the sovereign as any systemically important institution will eventually always be a liability of the state (society at large). Attempts, or rather promises, were made to confront this issue by allowing the ESM to lend to the banking system directly, rather than via the intermediary of the government. But while such a move was contemplated for Spain, it was fiercely opposed by some member states (eg Germany) and eventually did not come to fruition.

As other policy options failed to gain sufficient traction (or had, indeed, deleterious effects in the form of negative output growth), the ECB stepped Into this area too. Pivotal in its attempt to calm markets and provide breathing room to beleaguered governments was its announcement to purchase unlimited amounts of government securities with a maturity of up to three years if said government submitted to a troika-led adjustment program and stuck to it (though the ECB coyly justified its decision as “ensuring the proper functioning of the monetary transmission channel”). The boldness of this move was encapsulated in ECB president Draghi’s promise to do “whatever it takes” to save the euro.

This bold promise was instrumental in calming markets even though it had yet to be tested and executed. This test has now arrived. If the ESM is not to lend to banks directly and ECB liquidity provision is viewed as inappropriate for undercapitalized banks, (and widespread bank failures are deemed unacceptable) the solution is to let the government do the job and provide temporary monetary financing via ECB purchases. EZ policymakers and the ECB have failed to live up to this task and in this the Cyprus crisis bodes ill for future rescue attempts. Markets should be much more hesitant taking solace in the promise of future OMTs.

The other pillar in the effort to insulate failing, systemically important banks from the potentially insufficient capacity of the sovereign to rescue them (eg Iceland) was the project to socialise such costs in the common interest of the Eurozone. Such a ‘banking union’ requires common supervision, common resolution (funds) and common deposit insurance.

While progress towards agreement on any of those has been slow and uneven at best, this latest decision likely puts the nail in the coffin of the banking project. The cavalier discarding of official guarantees is disheartening in its own right. But beyond that, it also demonstrates a complete lack of the much-heralded European solidarity when national interests are in play. The idea of dealing with crises by establishing a well-understood resolution regime that lets governments write down the claims of uninsured creditors (remember Deauville?) has been turned on its head. As such, it makes a mockery of any EU declaration that professes to deal with the crisis in a systematic way. Against this backdrop, this latest way of dealing with the Eurozone crisis will reverberate far beyond this tiny island.