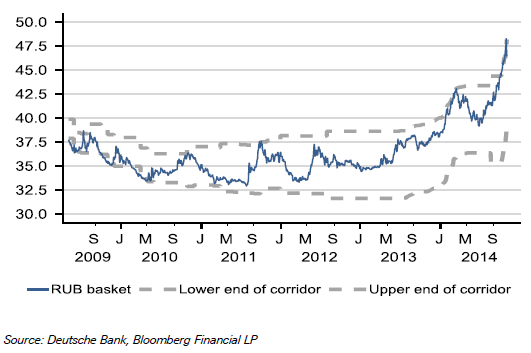

- Russia’s central bank yesterday abandoned its policy of unlimited FX intervention in support of the ruble. This precipitates the shift to a freely floating exchange rate regime which was due to commence only in 2015. The move came in response to continued capital outflows, which had led to a 35% decline against the USD since June, a $71 bn loss in reserves (-15%) from October 2013 and a rise in interest rates by 400bps to 9.50% since the start of the year.

The decision will have several consequences:

- Stem the slide in reserves: While the float may initially remain somewhat “dirty”, it will stop the bleeding of foreign reserves. There was no limit on reserve sales so far and the CBR is said to have intervened by as much as $2.5 bn a day. It will now spend no more than $350 mn per day (presumably to smooth volatility).

- Erase fear of capital controls: Rumours that capital controls might be imposed were themselves a driver of outflows. Such restrictions are not necessary under a floating FX regime and the capital drain due to this concern should thus slow.

- Take pressure off interest rates: When the exchange rate is fixed or managed, interest rates become “endogenous”, that is they must adjust to whatever level balances demand and supply for rubles in order to keep its price (the exchange rate) at the targeted level. Interest rates may still have to rise further to combat any rise in inflation (in real terms, they are at less than 1.5%), but in a less abrupt manner.

- Rising inflation: To the extent that a freer exchange rate regime translates into a weaker ruble, this may pass through to inflation (already at 8.1% yoy in September) through higher prices of imported goods. Two factors can mitigate this effect : in a demand recession, feedthrough is much more sluggish (eg Brazil’s 1999 experience) and the import content of the CPI basket must be declining due to economic sanctions. On the other hand, with the Russian economy not being able to generate perfect substitutes in the near term, the ensuing scarcity also drives prices up (this takes place regardless of the exchange rate).

- Boost fiscal and export revenues: Some 70% of Russia’s exports and 50% of its budgetary revenues derive from oil, which is priced in USD and has declined by over 20% since mid-year. For Russian exporters and the government, the slide of the ruble has more than compensated for the associated revenue loss though, helping revenues in local currency terms.

- Combat Dutch Disease: Excessive reliance on capital-intensive resource extraction tends to displace other economic activities, which typically have a lower rate of return. As the freeing of the exchange rate and the resulting depreciation make other industries more competitive again, this could reignite manufacturing activity if sustained in the medium term.

The effect of the exchange rate on the economy will be difficult to discern. It is only one piece of the puzzle and many other factors impinge on economic performance, not least the conflict in Ukraine, the associated economic sanctions and rise in inflation, the structural erosion of the twin surpluses and the fall in the price of oil, Russia’s main export earner. All else equal though, a controlled freeing of the exchange rate can liberate other levers of economic policy and, via looser monetary conditions, eliminate some of the economic distortions (pressure for capital outflows) weighing on output growth. Yet, Russia’s antagonistic foreign policy stance could instead further undermine investor confidence and lead to a vicious cycle of capital outflows -FX weakening – rising inflation – monetary tightening and lower growth.

UPDATE: Russia Relaxes Inflation Target

- The Russian central bank pushed back its 4% inflation target from 2016 to 2017 (current target 5%). On the one hand, this acknowledges the adverse effect of the recent slide of the ruble on inflation as well as the effect of sanctions on food prices; on the other hand it will loosen the CBR’s room for manoeuvre somewhat by requiring a less stringent policy response to the current rise in inflation (8.3% yoy in October).

- The inflation target has become the sole anchor for inflation expectations after the central bank precipitated its move to a freely floating exchange rate last week. . However, if the central bank hopes to regain the initiative from the market, this is more likely to backfire as a more relaxed target is unlikely to strengthen the credibility of its policy actions. Instead, with the central bank standing back both from its commitment to exchange rate stability and to price stability, the vicious cycle of depreciation/capital outflows could accelerate.

- The official statement can be found here and states amongst other things:

“Consumer prices were largely affected by the ruble depreciation. Foreign trade restrictions imposed in August 2014 and adverse markets conditions for certain food products spurred inflation as well. According to Bank of Russia estimates, inflation will in all probability exceed 8% till the end of 2014, i.e. it will significantly deviate from a 5% target. In this situation, it is important to continue pursuing the monetary policy aimed at slowing down consumer price growth.Our objective is to reduce inflation to 4% in the medium run. This is an ambitious goal. However, we are not trying to achieve it as soon as possible and at any cost. We plan to reduce inflation to the target gradually, taking into account the potential of the Russian economy. According to our estimates, in case the imposed trade restrictions remain effective, as announced, for a period of one year, and in the absence of new negative factors, consumer price growth will decline to 4% in 2017 with no significant slowdown of the economy.”