As the positions between the Greek government and the Troika harden, it appears that an agreement to extend the current bail-out program or secure some other form of official financing becomes ever more elusive. Yet, it is highly unlikely that the Syriza government will disengage from official financing, default or exit the Eurozone. Why? To put it succintly: Beggars can’t be choosers. For more, read on.

The issues involved are complex, but there are three key, powerful reasons that will ultimately compel the government to compromise.

- Economic Turnaround: Past government efforts to induce economic adjustment have just begun to bear fruit. Greece’s economy finally eked out some positive growth (1.6% yoy) in Q3 2014. At the same time, it managed to achieve a primary budget

surplus in excess of 2% of GDP in 2014 and its current account balance shifted from a 14% of GDP deficit in 2008 to a 1.4% of GDP surplus. All these achievements would be at risk, if the government failed to reach an agreement with its creditors (80% of which are official), defaulted or worse, withdrew from the Eurozone.

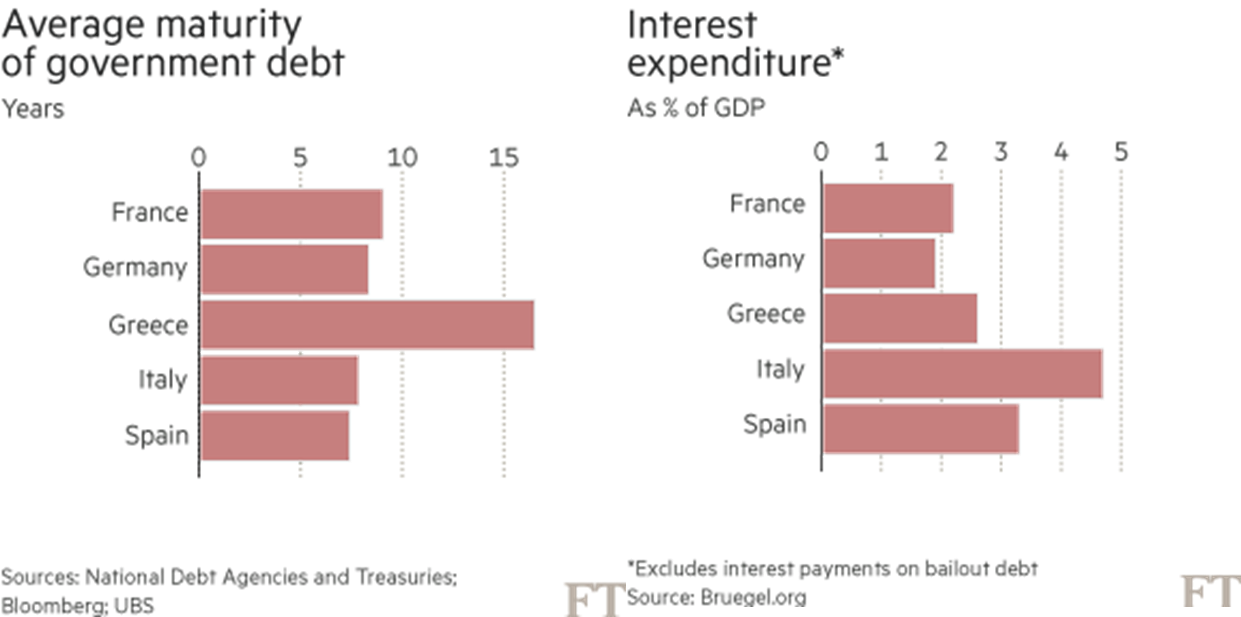

surplus in excess of 2% of GDP in 2014 and its current account balance shifted from a 14% of GDP deficit in 2008 to a 1.4% of GDP surplus. All these achievements would be at risk, if the government failed to reach an agreement with its creditors (80% of which are official), defaulted or worse, withdrew from the Eurozone. - Debt terms: Greece already enjoys extremely favourable terms on its debt following two previous reschedulings. The widely advertised public debt level of 175% of GDP may be unsustainable at current growth and inflation rates but belies a much more favourable underlying debt picture. For one, despite yields of 10-11% on its 10yr sovereign market debt, the actual interest rate Greece pays on its debt is much lower than that of any other program country and approaching levels of Germany. Previous restructurings reduced the rate on Troika loans from 300-400bps over Euribor to just 50bps, while EFSF loans carry a 0% rate. As a result, the effective rate paid is an average 2.6%, compared to the 2.2% France pays (see chart). And this doesn’t account for the interest payments it has made on bonds held by the ECB, which it is due to

receive back and which reduce the net rate even further. Second, the Troika previously extended Greece’s debt to 2041, while EFSF loans run for over 30 years. As a result, the average maturity of Greek debt is much longer than that of other Eurozone members in good standing at 16.5 years (see chart).

receive back and which reduce the net rate even further. Second, the Troika previously extended Greece’s debt to 2041, while EFSF loans run for over 30 years. As a result, the average maturity of Greek debt is much longer than that of other Eurozone members in good standing at 16.5 years (see chart). - ECB: The ECB holds the key to Greece’s fortunes as it has until recently bankrolled its banking system which experiences heavy deposit withdrawals (a reported Eur12 bn since November). To that end, the ECB had waived the usual requirements that collateral posted for access to ECB liquidity be at least investment grade. However, on

February 4, it withdrew this derogation on the basis that a successful conclusion of the current program review (a requirement) was unlikely. This forces Greek banks to turn to the Emergency Liquidity Assistance (ELA), operated by the Bank of Greece. But this too is subject to ECB approval and can be withdrawn subject to a 2/3 majority in the Governing Council.

February 4, it withdrew this derogation on the basis that a successful conclusion of the current program review (a requirement) was unlikely. This forces Greek banks to turn to the Emergency Liquidity Assistance (ELA), operated by the Bank of Greece. But this too is subject to ECB approval and can be withdrawn subject to a 2/3 majority in the Governing Council.

Finally, one can add to this list a conceptual point. There is a fair argument to be had over whether economies in recession should engage in expansionary fiscal policy in order to reignite activity. This type of Keynesian demand stimulus abstracts from balance sheet considerations and relies on the so-called multiplier effect of public spending. It is based on the premise that an economy can be made to “outgrow” its debt burden (through an increase in its denominator, the debt ratio would fall, all else being equal). However, numerous examples in the Eurozone and in Greece in particular have shown that this approach has failed and the debt burden has instead grown. When an economy is in a credit crisis and has lost market access, further fiscal expansion is ruinous. True, spending could be financed through tax increases (current or future) or asset sales as much as through debt. But the former would be self-defeating, while the latter is opposed by Greece’s new government.

Adjustment, although hard, thus remains the only viable solution. You don’t cure an alcoholic with more alcohol.