- China’s latest FX adjustment is neither a “competitive devaluation” nor the opening shot in a “currency war”. Given the negative contribution of net exports to growth as of late, it is also unrelated to efforts to boost growth.

- Instead, the weakening of the exchange rate represents the unavoidable resolution of a policy conflict which saw the PBoC simultaneously tighten (to maintain the FX regime) and ease monetary policy (to combat deflation). Conveniently, it also aligns the PBoC’s tools better with market principles.

- All China has to do now is to prevent the slide from becoming disorderly. For the moment, it has ample tools to do so.

The Chinese authorities decided to lower the reference USDCNY rate by 1.9% on August 11 and by a further 1.6% on August 12. Various reasons have been proposed to explain this unexpected move:

- The official explanation is that China is simply proceeding along the path of greater market liberalization, allowing its exchange rate ever greater freedom to float;

- More skeptical observers suggest an attempt to invigorate economic growth through a boost to exports which had declined during five of the past seven months, most notably by 8.3% yoy in July;

- Others regard the move as part of the campaign to attain inclusion in the SDR (Special Drawing Rights, whose composition the IMF Board is due to review in November.

Don’t Look Here

Starting from the back, it is true that China has never made any secret of its desire to attain reserve currency status. It treats this as a matter of national pride and as vindication of its status as a serious player on the global stage. And it regards inclusion of the remnimbi in the SDR, an accounting construct consisting of four currencies (the USD, EUR, JPY and EUR), as a stepping stone towards that goal (it is not in our view and largely of symbolic value). The IMF reviews the composition of this numeraire once every five years, with the next review coming up in November. To qualify for inclusion, a currency must be issued by a member whose exports of goods and services had the largest value over a five-year period and which has been determined by the Fund as being “freely usable”. In turn, this requires that the currency be 1) “widely used” to make payments for international transactions and 2) “widely traded” in principal exchange rate markets. This usage definition is different from the notion of a currency being floating freely or being fully convertible. However, a currency which meets the export criterion and is freely floating/convertible is more likely to be “widely used”. Convertibility and free float are neither necessary, nor sufficient for inclusion in the SDR, but they are critical to achieve reserve currency status. As such, the collateral effect of the currency move may come in handy for policymakers but was unlikely the primary driver of their decision.

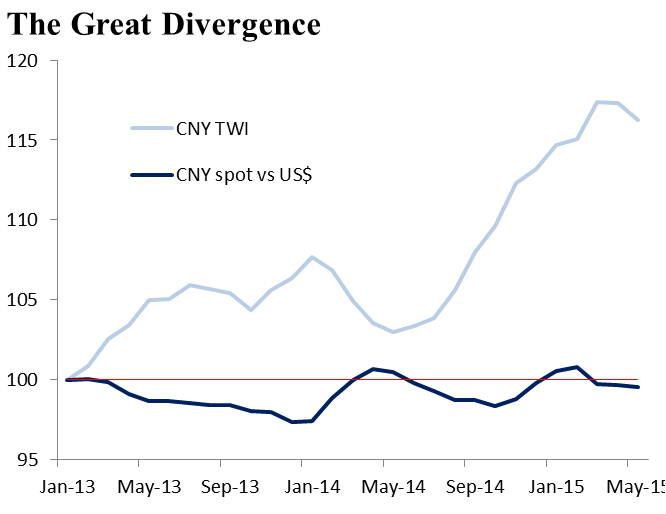

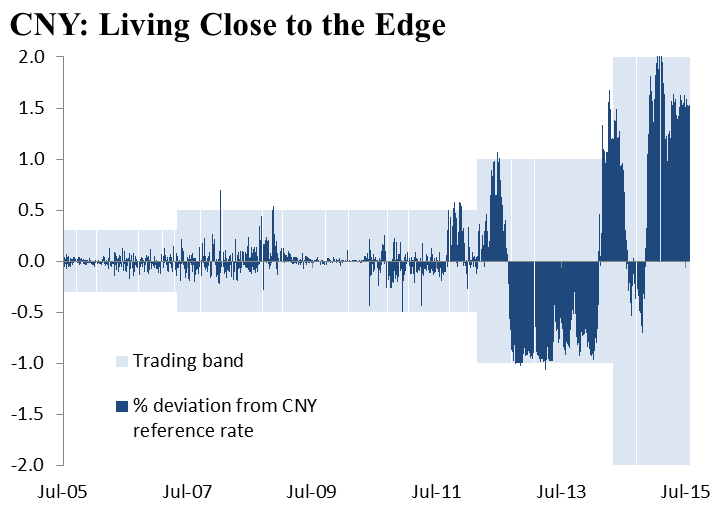

The second explanation is that after eight years of slowing growth (a post-crisis rebound excepted), insufficient progress in promoting private consumption as a key growth driver and years of wholesale price deflation, the government has engaged in a “competitive devaluation”. After all, merchandise exports fell 8.3% yoy in July, the fifth contraction this year and net exports have contributed little to GDP growth since 2012. It is at this point that many invoke the much-hyped term of “currency wars” and the idea that a new participant has entered this malicious but ultimately zero-sum game. In that respect it is important to recall the peculiarities of the Chinese currency regime. In 2005, the PBoC de-pegged the CNY from the USD, announcing that it would target an undisclosed currency basket instead and allowing the spot rate to float +/-0.3% around a pre-announced reference rate (the fluctuation band was subsequently widened three more times – in 2007, 2012 and 2014 – to an ultimate width of +/-2%). Since the de-peg the CNY has appreciated some 25% against the dollar, but the bilateral rate has remained fairly stabl e during the past two years. By contrast, given the appreciation of the USD and the CNY’s close relationship to it, the latter has appreciated by 70% in (real) trade-weighted terms over the same period, 15% of which took place over the past year. Allowing a 3.3% weakening of the reference rate (so far) is only beginning to unwind this run-up. While in 2005 China could be accused of manipulating its currency to keep it artificially cheap, 10 years and a 70% appreciation later this claim rings hollow.

e during the past two years. By contrast, given the appreciation of the USD and the CNY’s close relationship to it, the latter has appreciated by 70% in (real) trade-weighted terms over the same period, 15% of which took place over the past year. Allowing a 3.3% weakening of the reference rate (so far) is only beginning to unwind this run-up. While in 2005 China could be accused of manipulating its currency to keep it artificially cheap, 10 years and a 70% appreciation later this claim rings hollow.

Finally, the claim that China is merely advancing its plan of successive market liberalization cannot be taken at face value but probably has the most truth to it. Indeed, the authorities stated that they had changed the calculation method for the reference rate from a system in which it determines the reference rate on the basis of morning quotes by the main banks to one in which it is to be based on the previous day’s closing price. If this where literally to be the case, the exchange rate would effectively be market determined, in a sort of sticky and capped float. But in reality, there is a difference between the previous day’s closing price and the next day’s opening price, indicating where the authorities’ preferences lie. Just as in the case of the USD de-peg, implementation doesn’t quite follow announcement. But the change in methodology is nevertheless possibly the bigger news than the actual FX move.

Beware the ‘Impossible Trinity’

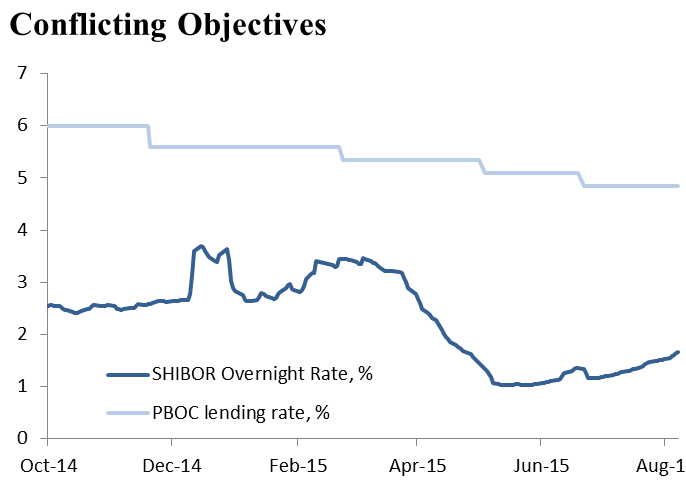

In all likelihood, China simply yielded to the unavoidable, a decision that is as opportunistic as it is strategic. It should be recalled that since Q4 2014, China has experienced capital outflows (and a drop in FX reserves from a high of almost $4.0 trn in June 2014 to $3.7 trn per June 2015) and that the spot rate has persiste ntly traded on the weak side of its +/-2% fluctuation band, often close to the edge. In turn, this required repeated intervention in the form of CNY purchases (USD sales) by the PBoC, which reduced liquidity and drove domestic money market rates up. This was in conflict with the PBoC’s desire to ease monetary policy (through its rate and RRR policy) in order to support a slowing economy.

ntly traded on the weak side of its +/-2% fluctuation band, often close to the edge. In turn, this required repeated intervention in the form of CNY purchases (USD sales) by the PBoC, which reduced liquidity and drove domestic money market rates up. This was in conflict with the PBoC’s desire to ease monetary policy (through its rate and RRR policy) in order to support a slowing economy.

To economists this conflict is known as the Impossible Trinity: the impossibility of simultaneously running a controlled exchange rate regime, with an open capital account, while maintaining full monetary sovereignty. The decision by the authorities to give in to market f orces – which exercised downward pressure on the exchange rate – conveniently not only helps on the above three objectives but, importantly, also resolves an inconsistency in the monetary policy mix. The PBoC now has all its policy levers pointing in the right direction, rather than tightening conditions with one hand (in the FX market) and easing them with the other (in the rates market).

orces – which exercised downward pressure on the exchange rate – conveniently not only helps on the above three objectives but, importantly, also resolves an inconsistency in the monetary policy mix. The PBoC now has all its policy levers pointing in the right direction, rather than tightening conditions with one hand (in the FX market) and easing them with the other (in the rates market).

Keep It There

As such, the move was not only expedient, but also necessary and to be welcomed. It is not a “competitive devaluation” or an opening shot in a “currency war”. But rather the unavoidable resolution of a policy conflict which better aligns its tools with market principles. The direction of the move is thus the right one. All China has to do now is to prevent the slide from becoming disorderly. For the moment, it has ample tools to do so.