- The global economy is facing its third deflationary shock in succession.

- After the US economy and the Eurozone, China is the epicenter of the latest crisis.

- The erstwhile Sino-American Symbiosis resurfaces in a new, more nefarious form. The causation runs from reserve declines, to global monetary tightening. to slowing credit expansion and private consumption. This process is only just beginning.

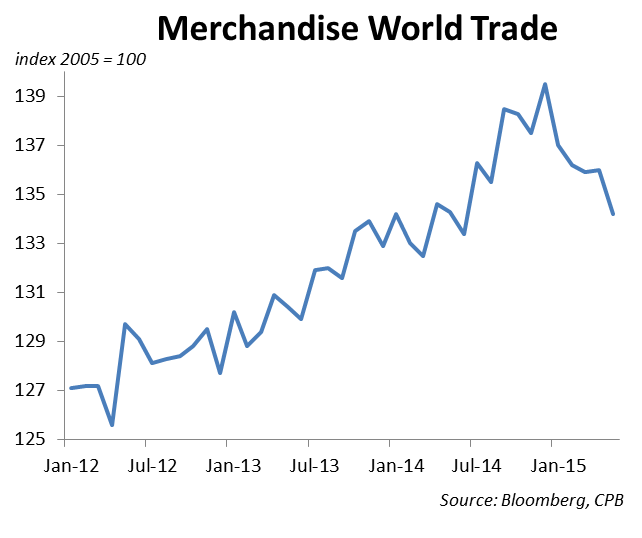

Now in its eighth year, the Great Financial Crisis is entering its third phase, which threatens to derail the global recovery once more. The first phase (2007-08), which was marked by the bursting of the US property bubble – with the sub-prime lending market at its core – was followed by a second phase (2011-12), which threatened the breakup of the Eurozone as Greece lost its availability to service its ballooning public debt. Now, the slowdown of China and other emerging markets (EMs) raises the specter of yet another disruption to global growth. While EM growth outperformance was as high as 8% in the immediate aftermath of the crisis breakout, it has dwindled  to some 2.5%. It is true that today the balance sheets of many EMs are much stronger than in the 1990s and their policy mix is more adaptable, notably because of the spread of floating or, at least, more flexible exchange rate regimes. As such, the problem many economies face is not that of an acute crisis due to unsustainable imbalances, but rather that of a chronic “growth crisis”, aggravated and characterised by the collapse in global trade.

to some 2.5%. It is true that today the balance sheets of many EMs are much stronger than in the 1990s and their policy mix is more adaptable, notably because of the spread of floating or, at least, more flexible exchange rate regimes. As such, the problem many economies face is not that of an acute crisis due to unsustainable imbalances, but rather that of a chronic “growth crisis”, aggravated and characterised by the collapse in global trade.

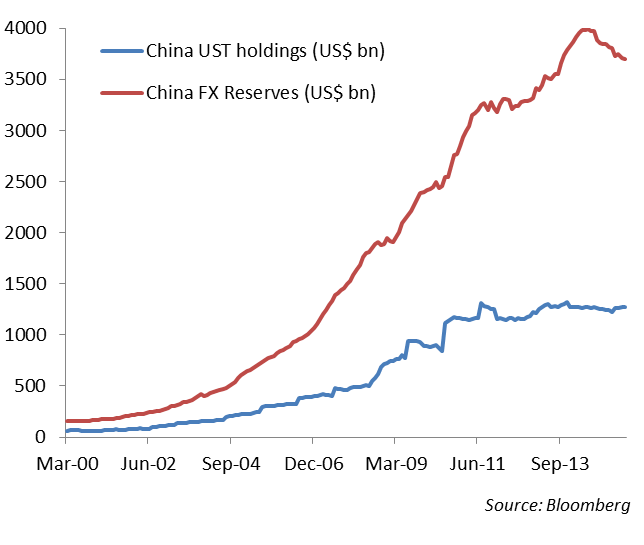

This matters as the US and Chinese economies remain in as symbiotic an embrace as ever. But it is one that is rather less benign than during the pre-crisis period when a widening US external deficit drove Chinese reserve accumulation, which in turn led to rising purchases of US Treasuries and kept a lid on US government yields (fueling credit expansion and consumption). Now, the rise in US rates coupled with a slowing Chines e economy threatens increasing capital outflows, which undermine China’s ability (or indeed, its need) to accumulate reserves and purchase US government securities. In turn, this exacerbates the tightening in US monetary conditions. China holds $1.3 trn (36.5% of total) of US Treasuries and sold more than $100 bn during its recent support operation for the renminbi. On the other hand, weaker Chinese demand has led to a sell-off in commodity prices, which benefits advanced economies importing raw materials.

e economy threatens increasing capital outflows, which undermine China’s ability (or indeed, its need) to accumulate reserves and purchase US government securities. In turn, this exacerbates the tightening in US monetary conditions. China holds $1.3 trn (36.5% of total) of US Treasuries and sold more than $100 bn during its recent support operation for the renminbi. On the other hand, weaker Chinese demand has led to a sell-off in commodity prices, which benefits advanced economies importing raw materials.

But EMs are also more generally intertwined with advanced economies, having benefited from massive liquidity expansions by G10 central banks since 2008. Capital flows in search of return flooded emerging markets, driving a credit-fuelled consumption boom there. Between 2007 and end-2014, EM credit rose from 50% of GDP to 127% of GDP, according to estimates by JP Morgan. The vast majority of credit was provided by banks, while on the borrower side, corporates accounted for three quarters of private non-financial debt (Asia registered both the fastest growth and the highest levels of debt). Banks are particularly sensitive to changes in funding costs and tighter monetary conditions may accelerate the outflow of capital from emerging markets, further pulling the rug from EM growth and thus DM export prospects.